Should General Motors Sunset Buick and GMC?

Streamlining is in order?

I believe General Motors (GM) should go on a diet, a major diet. Even having four brands, this is too many. In case you’re wondering if this is an anti-GM article, it’s not. Growing up, I was a GM fanboy and learned as much as I could about it. I grew up with Chevys, Cadillacs, and Buicks, so I bled General Motors. I think GM should focus on just 2 brands. This wouldn’t be much different from how Toyota and Honda are structured (Toyota is for the mass-market and Lexus is the luxury brand, Honda is the mass-market brand and Acura is the luxury brand).

General Motors, one of the ‘Big Three’ American automakers, has been firmly embedded in automotive history almost from the beginning. Founded in 1908, General Motors bought automakers, Oldsmobile, Buick, Cadillac, Oakland (later Pontiac), and then later, Chevrolet under one umbrella. In the 20s, it innovated ‘planned obsolescence’ by making design changes every year, making it more enticing for consumers to get the ‘latest and greatest before they would otherwise.

Source: Report on the Motor Vehicle Industry, Federal Trade Commission, 1939

What if All Auto Brands were Made in the Same Factory?

How Auto Dealers Might Address the Way Consumers get Around in the Future

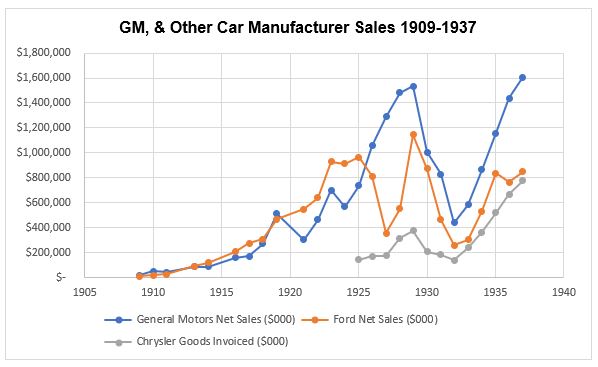

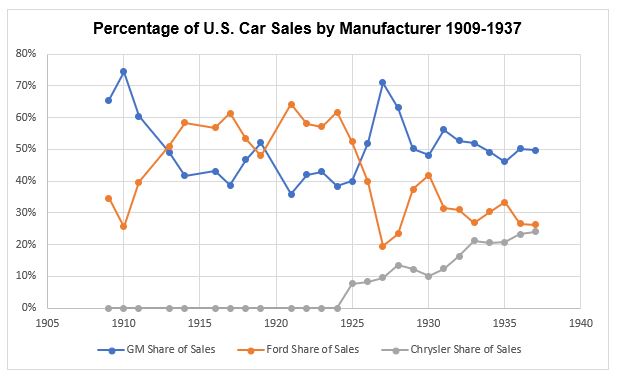

GM gets bigger…and then smaller

General Motors also mainstreamed building its cars on similar platforms in each of its brands but selling them with different trims, features, and price points. This worked well and helped GM maintain a large market share throughout much of the mid to late 20th century. This wouldn’t last long. Japanese automakers mounted fierce competition during the 70s and 80s. GM responded with the Saturn brand in 1985. By the 90s, GM had become this huge, unwieldy organization that did business in the areas of financial services, defense aerospace, and computer services.

Data source: Knoema

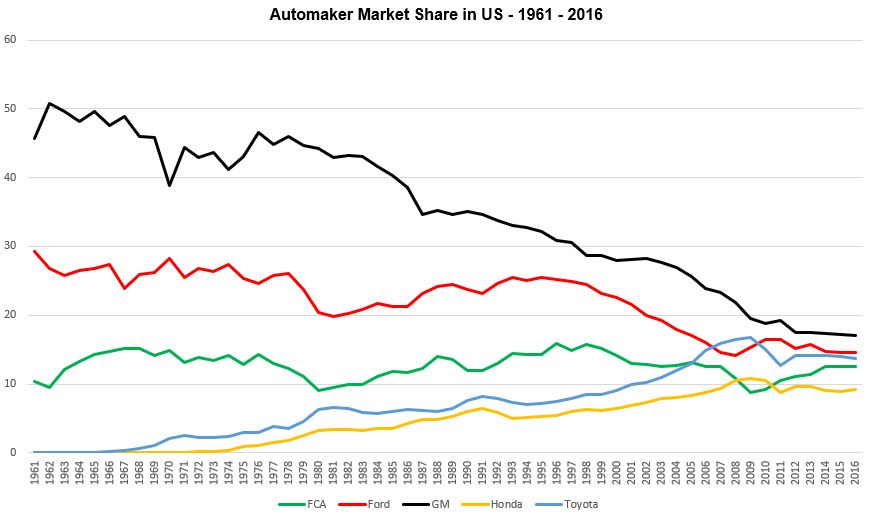

After selling off much of the non-automotive-related businesses in the late 90s, GM bought Saab and Hummer. It also put some money into Fiat, Subaru, and Suzuki. Things didn’t get better. After a few years of lackluster growth, GM killed off Oldsmobile in 2004. In 2008, Toyota became the world’s largest automaker. In 2010, two more of its brands ended up on the chopping block: Pontiac and Saturn. This left GM with Buick, Chevrolet, Cadillac, and GMC.

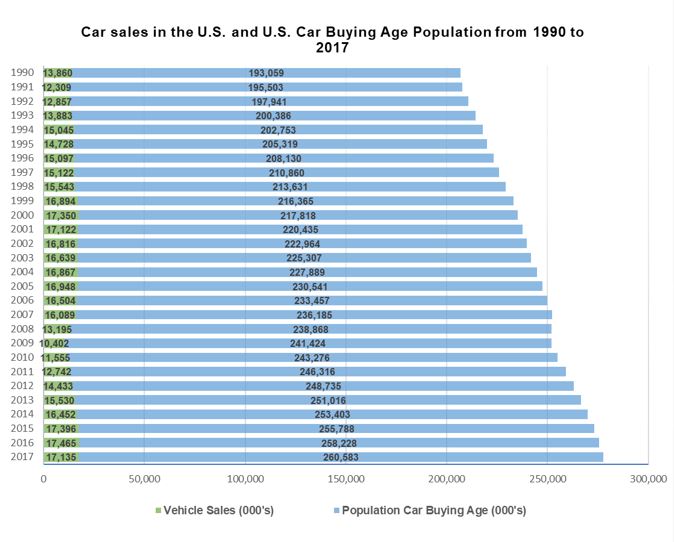

In a consumer environment where buying a new car is no longer an important part of the ‘American Dream’, people are increasingly preferring to be driven around in a stranger’s car or buy used vehicles. In this environment, it won’t take long for the red ink to flow. In 2017, GM lost nearly $4 billion. That year, Mary Barra, GM CEO said that the company would be overhauled. Part of this overhaul resulted in GM selling money-draining European car companies and introducing all-new crossover SUVs. The overhaul paid off: GM made $8.1 billion in 2018.

Why Should GM Get Smaller?

Toyota and Honda have done a great job of being profitable with just two brands each. “A volume brand and a premium brand can get the job done. Toyota has proven that,” said Karl Brauer, editor in chief of Edmunds.com, “Cadillac, Chevy, done.”

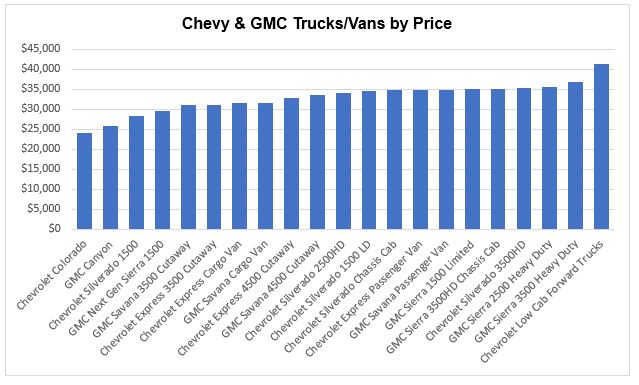

This might make some Chevy and GMC truck owners angry: there is essentially NO difference between the two trucks beyond minor styling and trim offerings. Chevy is positioned as the mainstream/volume brand and GMC as the premium brand. Pricing has become closer between the two brands over the years. If GM were to streamline its offerings, I believe Chevrolet and Cadillac should be the remaining brands.

Why keep GMC, when Chevy would do? Here’s an example of how close Chevrolet and GMC vehicles are, based on price:

Data source: General Motors

When looking at the number of GM brands, models, and average sticker prices, and comparing this to Toyota, there are some interesting takeaways:

- The average price of Chevrolet trucks and GMC trucks differ by $1,550.

- GM only has 6 more models than Toyota (this includes Lexus) (56 vs 50)

- The average price of all GM models is $35,705 compared to $43,797 for all Toyota models.

- There are almost as many Lexus models as there are Chevrolet models (25 vs 27) One-third of the Lexus models are hybrid versions.

- Chevrolet (volume brand) models come in with a higher average price than Buick (a near-premium brand), $33,393 vs $32,597, and both are less than the average price of GMC models ($35,111).

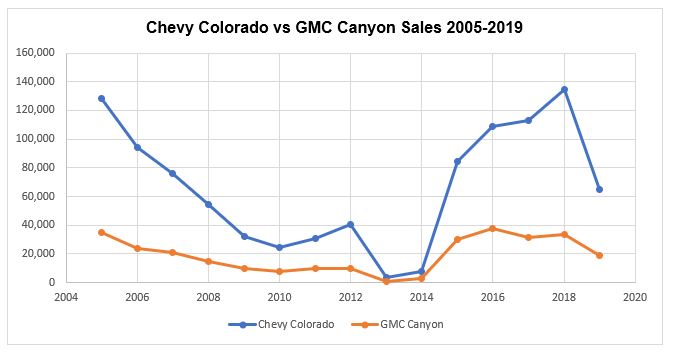

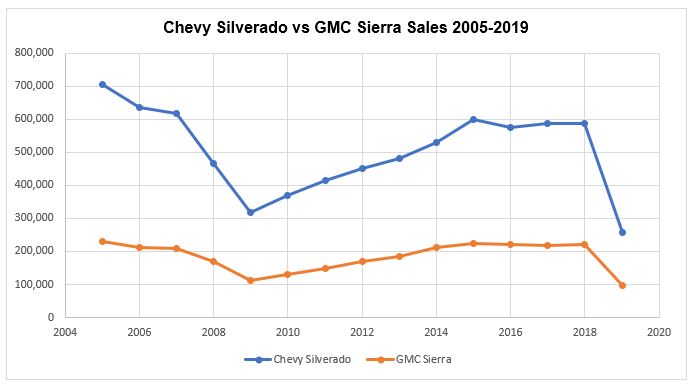

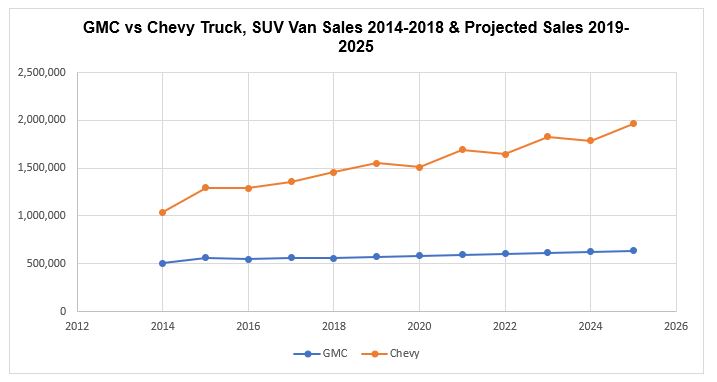

From 2005-2019, GM’s biggest sellers, Chevy trucks, vans & SUVs, and GMC, while essentially selling identical vehicles, couldn’t be any different when it comes to the number of sales. GMC Sierra sales averaged about 36% of Chevrolet Silverado sales. In comparison, GMC Canyon sales were 30% that of its cousin, Chevy Colorado. This suggests that many buyers see that the two brands are similar and decide to buy Chevy because of slightly lower price points. Based on sales data of the last five years, GMC vehicle sales are projected to remain flat over the next five years, while Chevrolet truck, van & SUV sales are projected to increase by about 26%.

Data source: GoodCarBadCar

Data source: GoodCarBadCar

Data source: GoodCarBadCar

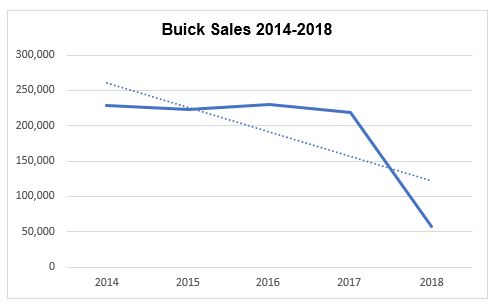

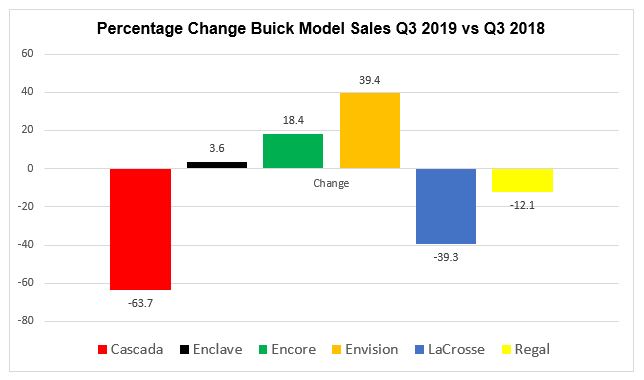

Buick sales dropped about 74% between 2017 and 2018. Half of its models saw sales declines between Q3 2018 and Q3 2019 (an average 38.36% decline). The models which saw sales increases during the same period were the Enclave, Encore, and Envision. These models saw an average sales increase of 20.46%. Buick sales between Q3 2018 and Q3 2019 declined by 17.9%.

Data source: GoodCarBadCar

Data source: GoodCarBadCar

Were Oldsmobile & Pontiac Popular?

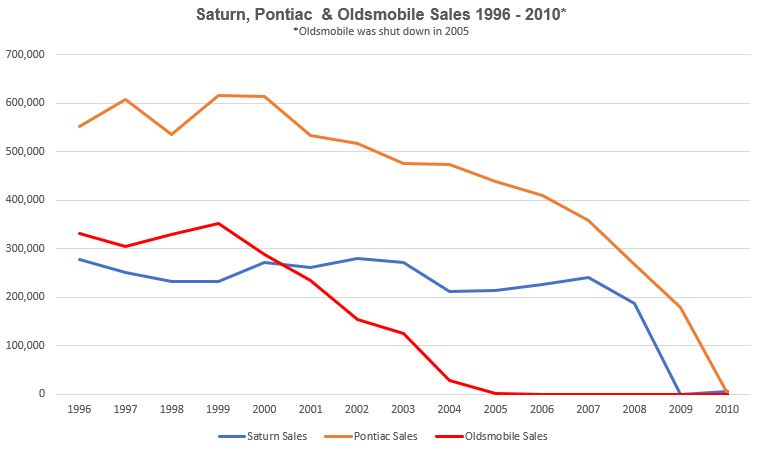

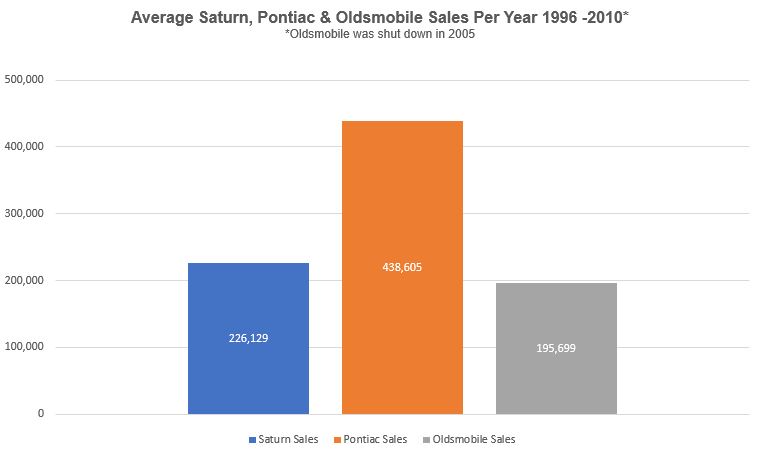

If you’re thinking Pontiac, Oldsmobile, and Saturn must have been ‘bad brands’ with terrible cars. You’d be wrong. In fact, these brands could hardly be considered sales laggards. Although between 1996-2010, Saturn, Pontiac, and Oldsmobile sales trended downward, this was true with just about any brand leading up to the great recession. During this period, Saturn sold an average of 226,000 cars each year, Pontiac sold about 439,000 cars and Oldsmobile sold 196,000 every year.

Data source: CarSalesBase

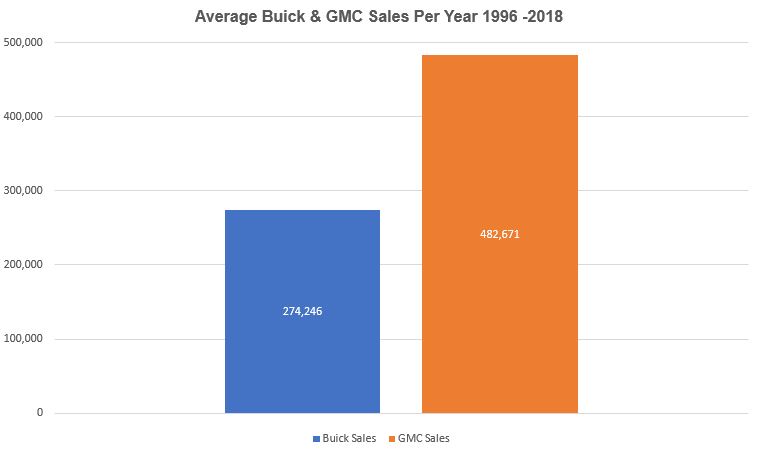

Saturn sold about 50,000 cars less per year than Buick’s 274,246 cars between 1996 and 2018. Pontiac sold about 44,000 fewer cars per year than GMC’s 482,671, during the same period. Even Oldsmobile, the brand that probably suffered the worst overall sales figures for a while, sold an average of more cars per year than Cadillac (196,000 vs 180,000).

Data source: CarSalesBase

Data source: CarSalesBase

So, sales were not the biggest factor in shuttering these brands. One of the things that helped make GM into the world’s largest automaker also became its liability. Consumers increasingly found GM’s business model of offering basically the same vehicle across each division, a turn-off. The sales started reflecting this dissatisfaction.

For example, one reason why Pontiac got the ax, is because it was essentially Chevrolet with sportier packaging. Oldsmobile was too much like Buick but less luxurious, but more so than Pontiac. GMC is basically an upscale Chevy truck, van, and SUV brand, and Buick is essentially a ‘near-luxury’ brand similar to Chevy ‘with Cadillac aspirations’. So, my proposal to kill off Buick and GMC isn’t too far-fetched. If GM could ax Pontiac, a brand that many consumers were passionate about, and one that sold relatively well, General Motors could certainly kill off GMC and Buick.